Exhibit 99.126

DEFI TECHNOLOGIES INC.

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2024

Dated: March 30, 2025

TABLE OF CONTENTS

| EXPLANATORY NOTES AND CAUTIONARY STATEMENTS | 1 |

| CORPORATE STRUCTURE | 3 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 4 |

| DESCRIPTION OF THE BUSINESS | 15 |

| Risk Factors | 25 |

| DIVIDENDS | 52 |

| DESCRIPTION OF SHARE CAPITAL | 52 |

| MARKET FOR SECURITIES | 53 |

| Escrowed securities | 53 |

| DIRECTORS AND OFFICERS | 54 |

| AUDIT COMMITTEE DISCLOSURE | 56 |

| PROMOTER | 57 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 57 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 58 |

| TRANSFER AGENT AND REGISTRAR | 58 |

| MATERIAL CONTRACTS | 58 |

| INTERESTS OF EXPERTS | 58 |

| ADDITIONAL INFORMATION | 58 |

i

EXPLANATORY NOTES AND CAUTIONARY STATEMENTS

Explanatory Notes

In this Annual Information Form (the “AIF”), the term “Company” or “DeFi Technologies” refers to DeFi Technologies Inc. and its subsidiaries as a whole, unless otherwise specified or the context otherwise requires.

Information contained in this AIF is given as of December 31, 2024, the financial year end of the Company, unless otherwise specifically stated.

Unless otherwise indicated, all currency amounts in this AIF and references to “$” are stated in Canadian dollars.

Market and industry data used throughout this AIF was obtained from various publicly available sources. Although the Company believes that these independent sources are generally reliable, the accuracy and completeness of such information are not guaranteed and have not been verified due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and the limitations and uncertainty inherent in any statistical survey of market size, conditions and prospects.

This AIF should be read in conjunction with the Company’s audited consolidated financial statements and management’s discussion and analysis for the financial year ended December 31, 2024. The financial statements and management’s discussion and analysis are available under the Company’s profile on the System for Electronic Document Analysis and Retrieval (“SEDAR+”) website at www.sedarplus.ca. The Company’s financial statements are prepared in accordance with International Financial Reporting Standards.

Caution Regarding Forward-Looking Information

This AIF contains “forward-looking information” within the meaning of that term under Canadian securities laws. This information relates to future events or future performance and reflects the Company’s expectations and assumptions regarding such future events and performance. Forward-looking information can be identified by the use of words such as, but not limited to, “plans”, “expects”, “project”, “predict”, “potential”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes” or variations (including negative variations) of such words and phrases, or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved.

In particular, all statements, other than statements of historical facts, included in this AIF that address activities, events or developments that management of the Company expects or anticipates will or may occur in the future contain forward-looking information, including but not limited to, statements with respect to:

| ● | financial, operational and other projections and outlooks as well as statements or information concerning future operation plans, objectives, performance, revenues, growth, acquisition strategies, profits or operating expenses of the Company and its subsidiaries; |

| ● | details and expectations regarding the Company’s investments in the decentralized finance (“DeFi”) industry and the Company’s Equity Investments in Digital Assets (as defined herein); |

| ● | expectations regarding revenue growth due to changes in the Company’s business strategy; |

| ● | expansion and growth of the Company’s Asset Management, Ventures and Infrastructure business lines; |

| ● | development of ETPs and partnerships and joint ventures with other companies; |

| ● | growth of assets under management (“AUM”); |

| ● | listing of ETPS; |

| ● | identifying and capitalizing on low-risk arbitrage opportunities within the digital asset market; |

| ● | digital asset staking, lending or trading transactions; |

| ● | listing of the Common Shares on Nasdaq; |

| ● | the AsiaNext MOU; |

| ● | the NSE MOU; |

1

| ● | SolFi Technologies; |

| ● | CoreFi Technologies; |

| ● | anticipated lending and staking income and management fees charged on ETPs; |

| ● | hedging activities; |

| ● | investment performance of ETPs, DeFi protocols and digital assets underlying ETPs and portfolio companies that the Company has invested in; |

| ● | future development of laws and regulations governing the DeFi industry; |

| ● | requirements for additional capital and future financing options; |

| ● | publishing and marketing plans; |

| ● | the availability of attractive investments that align with the Company’s investment strategy; |

| ● | future outbreaks of infectious diseases; |

| ● | the impact of climate change; and |

| ● | other expectations of the Company. |

Forward-looking information involves various risks and uncertainties. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Important factors that could cause actual results to differ materially from the Company’s expectations are described in the Company’s documents filed from time to time with the applicable regulatory authorities and such factors include, but are not limited to, risks related to the staking and lending of cryptocurrencies, DeFi protocol tokens, or other digital assets; risks relating to momentum prising and volatility of cryptocurrencies, DeFi protocol tokens, and other digital assets; cybersecurity threats, security breaches and hacks; the relative novelty of cryptocurrency exchanges and other trading venues; regulatory risks; hedging risk; the U.S. classification of crypto assets and the Investment Company Act of 1940; the issuance of crypto ETPs in the EU and non-EU countries; risk related the Company’s Ventures portfolio exposure; risks associated with banks cutting off services to businesses that provide cryptocurrency related services; the impact of geopolitical events; the further development and acceptance of digital and DeFi networks; risks and uncertainties associated with custodians of digital assets; risk of loss, theft or destruction of cryptocurrencies; risks associated with the irrevocability of transactions; risks associated with the potential failure to maintain the cryptocurrency networks; risks associated with the potential manipulation of blockchain; risks that miners may cease operations; risks related to insurance; risks related to the concentration of investments; risks related to competition; risk related to investments in private issuers and illiquid securities; risks related to cash flow, revenue and liquidity; risks related to the Company’s dependence on management personnel; risks related to macro-economic conditions; risks related to the availability or opportunities and competition for investments; risks related the share prices of investments; risks related to additional financing requirements; risks related to the return on investments; risks related to the management of the Company’s growth; social , political, environmental, and economic risks in the countries in which the Company’s investment interests are located; risks related to the due diligence process undertaken by the Company in connection with investment opportunities; risks related to exchange-rate fluctuations; risks related to non-controlling interests; risks related to changes in legislation and regulations; risks associated with the Company’s limited operating history and no history of operating revenue and cash flow; risks associated with the Company having limited cash flow and funds in reserve which may not be sufficient to fund its ongoing activities at all times; risks associated with conflicts of interest; risks associated with the volatility of the Common Shares market price; risks associated the future dilution of shareholders interest in the Company; and risks associated with the Company’s history of never paying dividends; and other risks described herein including under the heading “Risk Factors – Risks Relating to the Business and Industry of the Company”.

When relying on forward-looking information to make decisions, readers should ensure that the preceding information, the risks and uncertainties described in “Risk Factors” and the other contents of this AIF are all carefully considered. The forward-looking information contained herein is current as of the date of this AIF, and, except as may be required by applicable law, the Company disclaims any obligation or undertaking to publicly release any updates or revisions to any forward-looking information contained herein to reflect any change in expectations, estimates and projections with regard thereto or any changes in events, conditions or circumstances on which any information is based. Readers should not place undue importance on such forward-looking information and should not rely upon this information as of any other date. In addition to the disclosure contained herein, for more information concerning the Company’s various risks and uncertainties, please refer to the Company’s public filings available under its profile on SEDAR+ at www.sedarplus.ca and at www.cboe.ca.

With regard to all information included herein relating to companies in the Company’s Venture portfolio, the Company has relied on information provided by the investee companies and on publicly available information disclosed by the respective companies.

2

CORPORATE STRUCTURE

Name, Address and Incorporation

The Company was incorporated in British Columbia pursuant to the Company Act (British Columbia) (the “BCCA”) under the name “Western Premium Resource Corp.” on April 14, 1986. On August 29, 1997, the Company filed a certificate of change of name under the BCCA and changed its name to “Zodiac Exploration Corp.” On December 18, 1998, the Company filed a certificate of change of name under the BCCA and changed its name to “Donnybrook Resources Inc.” On August 13, 2003, the Company filed a certificate of change of name under the BCCA and changed its name to “Rodinia Minerals Inc.” On November 3, 2009, the Company was continued under the Business Corporations Act (Ontario) (the “OBCA”), and on June 15, 2010, the Company filed articles of amendment under the OBCA and changed its name to “Rodinia Lithium Inc.” On August 16, 2016 the Company filed articles of amendment under the OBCA and changed its name to “Routemaster Capital Inc.” The common shares of the Company (the “Common Shares”) began trading on the TSX Venture Exchange (the “TSXV”) on June 30, 2010. The Company sold its sole subsidiary on December 29, 2015 and completed a change of business (“COB”) to a tier 2 investment issuer under the rules of the TSXV on September 16, 2016. On January 19, 2021, the Common Shares were uplisted to trade on the Cboe Canada Exchange (formerly NEO Exchange Inc.) (“Cboe Canada”), and on February 26, 2021, the Company filed articles of amendment under the OBCA and changed its name to “DeFi Technologies Inc.” On April 19, 2022, the Common Shares were listed for trading on the OTCQB Venture Market. On June 1, 2022, the Company filed articles of amendment under the OBCA and changed its name to “Valour Inc.” On July 10, 2023, the Company filed articles of amendment under the OBCA and changed its name to “DeFi Technologies Inc.” The Company’s head office and registered office is located at Suite 2400, 333 Bay Street, Toronto, Ontario, M5H 2T6.

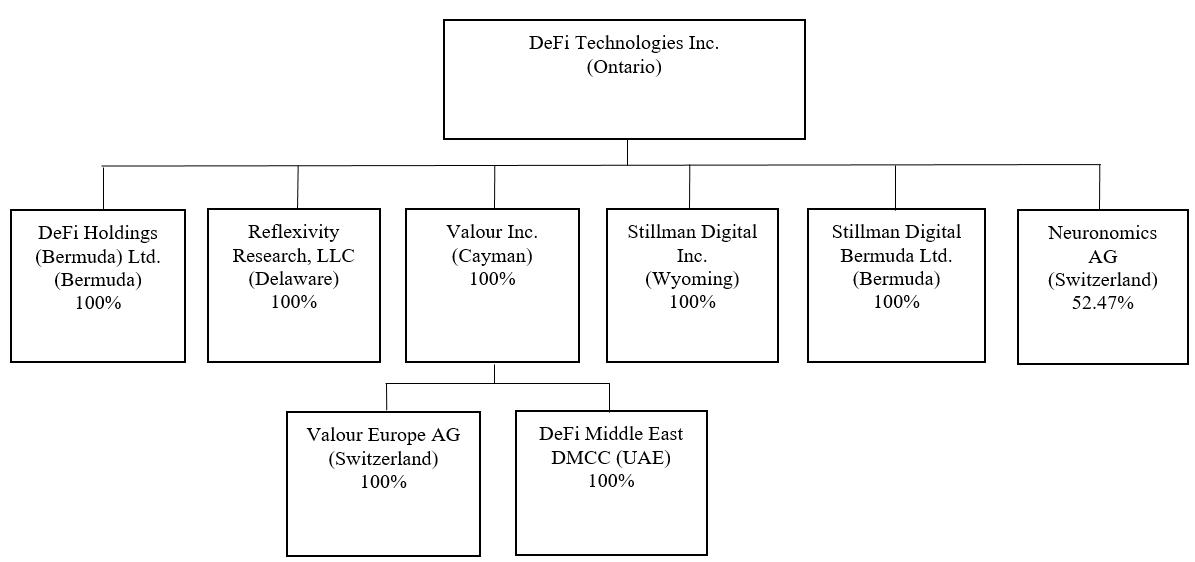

As of the date of this AIF, the Company holds 100% of DeFi Holdings (Bermuda) Ltd., 100% of Reflexivity Research, LLC (“Reflexivity Research”), 100% of Valour Inc. (“Valour Cayman”), 100% of Stillman Digital Inc. (“SDI”), 100% of Stillman Digital Bermuda Ltd. (“SDB” and together with SDI “Stillman Digital”) and 52.47% of Neuronomics AG. The following is an organizational chart illustrating the inter-corporate relationships between the Company and its subsidiaries and the jurisdiction of organization of each such entity, as at the date hereof:

Note: Valour Digital Securities Limited (“VDSL”), is owned by the charitable trust VLR Charitable Trust in Jersey. VDSL and Valour Cayman are together referred to as “Valour”. Defi Capital Inc. and Electrum Streaming Inc., wholly-owned subsidiaries of the Company, are in the process of being dissolved.

3

GENERAL DEVELOPMENT OF THE BUSINESS

The Company is a publicly listed company on Cboe Canada trading under the symbol “DEFI”. The Company operates five lines of business: Asset Management, Ventures, DeFi Alpha, Reflexivity Research and Stillman Digital, each of which is explained further below under their respective headings in “Description of Business”.

Three Year History

The following is a summary of the general development of the Company’s business over the three most recently completed financial years.

Subsequent to Fiscal 2024

On March 3, 2025, the Company announced that Valour launched four new ETPs on the Frankfurt Exchange: Valour Dogecoin (DOGE) EUR, Valour Aptos (APT) EUR, Valour Sui (SUI) EUR, and Valour Render (RENDER) EUR.

On March 3, 2025, the Company announced that it had appointed Chase Ergen to the board of directors of the Company (the “Board”). Mr. Ergen is a visionary entrepreneur and a leading figure in the decentralized finance space. As the son of Charlie Ergen, founder of Dish Network, a subsidiary of Echostar (NASDAQ: SATS), Chase has leveraged his firsthand experience, entrepreneurial roots, and forward-thinking mindset to drive innovation across satellite technology, information and communications technology (ICT), and cross-sector enterprises. Mr. Egegn’s appointment follows the resignation of Krisztian Toth from the Board who will transition into an advisory role.

Fiscal 2024

Asset Management

In the year ending December 31, 2024 (“Fiscal 2024”) Valour announced the launch of the following ETPs:

| Date | ETP | Exchange | ||

| February 20, 2024 | 1Valour Internet Computer Physical Staking | Deutsche Börse Xetra and Gettex | ||

| February 22, 2024 | Valour Ripple (XRP) SEK | Spotlight Exchange | ||

| February 22, 2024 | Valour Binance (BNB) SEK | Spotlight Exchange | ||

| March 18, 2024 | 1Valour STOXX Bitcoin Suisse Digital Asset Blue Chip | Deutsche Börse Xetra, Gettex and Frankfurt Exchange | ||

| April 18, 2024 | Valour Short Bitcoin (SBTC) SEK | Spotlight Exchange | ||

| May 13, 2024 | Valour Internet Computer (ICP) SEK | Spotlight Exchange | ||

| May 13, 2024 | Valour Toncoin (TON) SEK | Spotlight Exchange | ||

| May 13, 2024 | Valour Chainlink (LINK) SEK | Spotlight Exchange | ||

| May 15, 2024 | Valour Bitcoin Staking (BTC) SEK | Spotlight Exchange | ||

| June 4, 2024 | 1Valour STOXX Bitcoin Suisse Digital Asset Blue Chip | Deutsche Börse Xetra and Frankfurt Exchange | ||

| June 18, 2024 | Valour Bitcoin Staking (BTC) EUR | Frankfurt Exchange | ||

| June 19, 2024 | Valour Hedera (HBAR) | Frankfurt Exchange | ||

| June 28, 2024 | Valour Hedera (HBAR) SEK | Spotlight Exchange | ||

| June 28, 2024 | Valour Core SEK | Spotlight Exchange | ||

| July 17, 2024 | Valour Near SEK | Spotlight Exchange |

4

| September 30, 2024 | Valour Ethereum Physical Staking | London Stock Exchange, Deutsche Börse Xetra, Gettex and Frankfurt Exchange | ||

| October 10, 2024 | Valour Sui (SUI) SEK | Spotlight Exchange | ||

| October 30, 2024 | Valour Bittensor (TAO) SEK | Spotlight Exchange | ||

| November 5, 2024 | 1Valour Bitcoin Physical Staking | Deutsche Börse Xetra | ||

| November 26, 2024 | Valour Dogecoin (DOGE) SEK | Spotlight Exchange | ||

| December 12, 2024 | Valour Sei (SEI) | Spotlight Exchange | ||

| December 12, 2024 | Valour Worldcoin (WLD) | Spotlight Exchange | ||

| December 12, 2024 | Valour Aptos (APT) | Spotlight Exchange | ||

| December 12, 2024 | Valour ASI (FET) | Spotlight Exchange | ||

| December 12, 2024 | Valour Render (RENDER) | Spotlight Exchange | ||

| December 12, 2024 | Valour Aerodrome Finance (AERO) | Spotlight Exchange | ||

| December 12, 2024 | Valour Arweave (AR) | Spotlight Exchange | ||

| December 12, 2024 | Valour Injective (INJ) | Spotlight Exchange | ||

| December 12, 2024 | Valour Aave (AAVE) | Spotlight Exchange | ||

| December 12, 2024 | Valour Pendle (PENDLE) | Spotlight Exchange | ||

| December 12, 2024 | Valour Fantom (FTM) | Spotlight Exchange | ||

| December 12, 2024 | Valour Kaspa (KAS) | Spotlight Exchange | ||

| December 12, 2024 | Valour Pyth Network (PYTH) | Spotlight Exchange | ||

| December 12, 2024 | Valour Jupiter (JUP) | Spotlight Exchange | ||

| December 12, 2024 | Valour Lido DAO (LDO) | Spotlight Exchange | ||

| December 12, 2024 | Valour Wormhole (W) | Spotlight Exchange | ||

| December 12, 2024 | Valour THORChain (RUNE) | Spotlight Exchange | ||

| December 12, 2024 | Valour Akash Network (AKT) | Spotlight Exchange | ||

| December 12, 2024 | Valour Starknet (STRK) | Spotlight Exchange | ||

| December 12, 2024 | Valour Metis (METIS) | Spotlight Exchange | ||

| December 18, 2024 | 1Valour Hedera Physical Staking | Euronext Amsterdam |

On November 22, 2024, the Company announced that Valour had entered into a memorandum of understanding with Asia Digital Exchange Ptd. Ltd. (“AsiaNext”) and SovFi inc. (“SovFi”) (the “Asia Next MOU”). AsiaNext, a global digital asset exchange regulated by the Monetary Authority of Singapore, bridges Asia and Europe by providing institutional investors with secure access to digital assets. It is backed by Japan’s SBI Digital Asset Holdings and SIX Group in Switzerland. The Asia Next MOU with Valour will evaluate and facilitate the listing and trading of Valour’s ETPs on AsiaNext’s securities exchange, enhancing AsiaNext’s position as a leading marketplace for institutional investors.

On August 6, 2024, the Company announced that Valour had entered into a memorandum of understanding with the Nairobi Securities Exchange (“NSE”) and SovFi (the “NSE MOU”). The key objectives of the NSE MOU include facilitating the creation, issuance, and trading of digital asset ETPs on the NSE by leveraging Valour’s extensive expertise in digital assets and ETPs. The NSE MOU aims to deploy financial products developed by Valour and SovFi, develop market infrastructure and enhance market access to global capital through tokenized finance primitives and real-world assets.

On June 11, 2024, the Company announced that it has deployed a Core Chain validator node to act as an independent validator for the network. The Company also staked 1,498 BTC on the Core Chain.

On April 8, 2024, the Company announced that Valour has launched a trading desk in the United Arab Emirates.

In Fiscal 2024, Valour invested US$61,741,683 in three tranches of a private investment fund designed to acquire Solana and Avalanche tokens from a bankrupt company (“Fund A”). The Company’s investment represents the acquisition of 491,249 Solana at US$105 per Solana and 931,446 Avalanche at US$11 per Avalanche.

The Solana acquired by the Company is locked and staked, earning staking rewards during the lock period. Staking rewards will accrue while Solana is locked and will become distributable on the same unlocking schedule as the Solana. The Solana will be released in monthly increments from January 2025 through January 2028.

The Avalanche acquired by the Company is locked and staked, earning staking rewards during the lock period. Staking rewards will accrue while Avalanche is locked and will become distributable on the same unlocking schedule as the Avalanche. The Avalanche will be released in weekly increments July 10, 2025 and continuing through July 1, 2027.

5

The investment in the investment fund was valued based on the latest available net asset value, as determined by the investment fund’s administrator less DLOM. The fair values of the investments were remeasured based on monthly valuation reports provided to the Company by the investment fund administrator.

In Fiscal 2024, Valour invested $153,516,846 (US$112,072,453) in two tranches of a private investment fund designed to acquire Solana tokens from a bankrupt company (“Fund B” and together with Fund A the “Equity Investments in Digital Assets”).

The Company’s investment represents the acquisition of 1,123,360 Solana at US$100 per Solana. The Solana acquired by the Company is locked and staked, earning staking rewards during the lock period and thereafter until such Solana is sold by the fund manager or an in-kind distribution in the limited partners of the fund. Staking rewards will accrue while Solana is locked and will become distributable on the same unlocking schedule as the Solana. Approximately 25 % of the Solana will be released in March 2025, while the remaining 75% of the Solana will be released linearly monthly until January 2028. The investment in the investment fund was valued based on the latest available net asset value, as determined by the investment fund’s administrator less DLOM. The fair values of the investments were remeasured based on monthly valuation reports provided to the Company by the investment fund administrator.

DeFi Alpha

On July 16, 2024, the Company announced that DeFi Alpha generated an additional approximately C$4.0 million (US$2.9 million) in USDT and C$15.3 million (US$11.2 million) in digital asset inventory through low-risk arbitrage trades in Q3 2024.

On June 3, 2024, the Company announced that its new business line, DeFi Alpha generated an additional C$59.2 million (US$43.4 million) from low-risk arbitrage trades. In its first few months since formation, DeFi Alpha generated approximately C$113.8 million (US$83.4 million). Of the US$83.4 million generated, US$19.5 million was used to pay down debt.

Reflexivity Research

On September 13, 2024, the Company announced that Reflexivity Research was holding its inaugural Crypto Investor Day in New York City on October 25, 2025.

On June 24, 2024, the Company announced that Reflexivity Research has partnered with CoinMarketCap, the world’s largest crypto pricing and data aggregator, to educate users on various digital assets with in-depth fundamental research. Through this partnership, CoinMarketCap users will now have access to Reflexivity Research’s high-quality, actionable research on individual digital assets, including fundamental analysis, market structure updates, and technical breakdowns.

On March 7, 2024, the Company announced that Reflexivity Research was holding its inaugural Bitcoin Investor Day on March 22, 2024 in New York City. The Bitcoin Investor Day, orchestrated by Reflexivity Research, aims to assemble hundreds of institutional investors, capital allocators, and forward-thinking entrepreneurs.

On January 9, 2024, the Company announced that it had entered into a binding letter of intent to acquire Reflexivity Research (the “Reflexivity Acquisition”). Reflexivity Research, co-founded by Anthony Pompliano and Will Clemente, offers high-quality crypto-native research designed for traditional finance investors. The firm is known for unique bitcoin analysis, along with counting some of the most well-known cryptocurrency organisations as clients, including eToro, Solana, Avalanche, NEAR, Fantom, Sei Network, and many more. Reflexivity Research’s research is distributed via their homepage, a premium membership portal, and an email list of over 55,000 investors. On February 7, 2024, the Company announced that it had completed the Reflexivity Acquisition.

6

Partnerships and Acquisitions

On December 10, 2024, the Company announced that it has signed a letter of intent to increase its holdings of Neuronomics AG (“Neuronomics”), a Swiss asset management firm specializing in quantitative trading strategies powered by artificial intelligence, computational neuroscience, and quantitative finance, to 10%. On March 7, 2025, the Company announced that it had further increased its stake in Neuronomics to 52.5%.

On November 14, 2024, the Company announced the launch of CoreFi Strategy Corp (“CoreFi Strategy”). Modeled after MicroStrategy and MetaPlanet’s successful approaches, CoreFi Strategy offers a regulated, leveraged pathway to Bitcoin yield and CORE—the native asset of the Core blockchain, designed to unlock sustainable Bitcoin yield and other key functions. On February 4, 2025, DeFi entered a binding letter agreement with CoreFi Strategy and Orinswift Ventures (the “CoreFi LOI”) to facilitate a reverse takeover (the “RTO”). The RTO will be completed through a definitive agreement that is to be negotiated by the parties, which will contain customary representations and warranties for similar transactions, and is expected to be structured as a three-corned amalgamation whereby a newly incorporated subsidiary of Orinswift will amalgamate with CoreFi, resulting in Orinswift acquiring all securities of CoreFi, and CoreFi securityholders becoming securityholders of Orinswift, as the resulting issuer following closing of the Transaction (the “Resulting Issuer”). The final structure for the Transaction is subject to satisfactory tax, corporate and securities law advice for each of Orinswift, CoreFi, and DeFi. Pursuant to the LOI the Core Foundation will contribute US$20 million in CORE Tokens to strengthen CoreFi’s treasury in exchange for 30% of the Resulting Issuer. Additionally, CoreFi plans to raise US$20 million in concurrent financing to accelerate its growth in Bitcoin Finance (BTCfi) technologies. DeFi will provide advisory services, intellectual property development and intellectual property licenses in exchange for 30% of the Resulting Isser.

On November 12, 2024, the Company announced the launch of SolFi Technologies, new pure-play investment vehicle dedicated to providing traditional investors with specific access to the expanding Solana (“SOL”) ecosystem. SolFi Technologies aims to generate consistent cash flow at higher yields than third-party staking providers, with these yields reinvested or distributed to its shareholders as dividends, enhancing returns and compounding growth. As a cornerstone shareholder and partner, the Company will benefit from increased exposure to Solana’s performance, unlocking new growth potential and revenue streams that complement its existing portfolio. SolFi Technologies is designed to act as a “MicroStrategy for Solana,” providing leveraged access to Solana’s high-yield staking and capital appreciation potential. Through innovative capital structures unavailable to ETFs, SolFi offers investors both token upside and cash flow opportunities, capitalizing on Solana’s rapid adoption and enabling investors to potentially outperform the underlying asset.

On July 30, 2024, the Company announced that it has entered into a strategic partnership with Zero Computing, a pioneer in verifiable computation on Ethereum and Solana. This partnership aims to build critical infrastructure to enhance the arbitrage discovery and execution capabilities of DeFi Alpha, and advance capabilities for capturing zero-knowledge enabled Maximal Extractable Value.

On July 9, 2024, the Company announced that it has signed a letter of intent to acquire Stillman Digital (the “Stillman Acquisition”). Stillman is a leading global liquidity provider offering industry-leading trade execution, settlement, and technology services. On October 7, 2024, the Company announced that it had completed the Stillman Acquisition.

Financial Statements and Auditor Matters

On September 6, 2024, the Company announced that it has refiled its 2023 annual consolidated financial statements (the “Refiled 2023 FS”) to include an amended auditor’s report delivered by HDCPA Professional Corporation (the “Auditors”). The date of the 2023 FS remains unchanged and the Refiled 2023 FS have not been restated in any respect. In connection with a continuous disclosure review by the Ontario Securities Commission, the Company determined to refile the Auditors’ report on the Company’s previously filed 2023 annual consolidated financial statements (the “Original 2023 FS”) to correctly identify the period over which the Auditors are providing assurance. The Refiled 2023 FS include an amended Auditors report which (a) identifies that the Auditors did not audit or express an opinion on the Company’s 2022 financial statements, (b) corrects a typographical error in the “Other Matters” section to refer to “December 31, 2023”, and (c) adds certain note references under “Description of the Key Audit Matter”.

7

On April 1, 2024, the Company announced that it has filed its financial statements of the Company for fiscal-year 2023 with restated comparative information for fiscal 2022 and the corresponding management’s discussion and analysis. The Company became aware of an enforcement report issued by the Canadian Public Accountability Board (“CPAB”) on December 7, 2023 against BF Borgers CPA PC (“Former Auditor”) (the “Enforcement Report”) resulting from an engagement findings report dated October 12, 2023 (the “CPAB Report”). As a result of the Enforcement Report, the Auditor provided a consultation with respect to the CPAB Report, remediation plan requested by CPAB and the impact on the scope of the audit for fiscal 2023 (the “Consultation”), As a result of the Consultation, the Company reassessed the application of IFRS on the accounting the valuation of the Company’s holdings in 3iQ and AMINA Bank AG (formerly SEBA Bank AG) as well as the valuation of Valour’s Genesis loan and collateral posted to secure such loan. Compared with the previously filed fiscal 2022 financial statement of the Company, the Amended and Restated Financial Statements reflected a (i) reduction in digital assets by $2,433,348 to $104,148,728 as at December 31, 2022; and (ii) reduction in private investments, at fair value through profit and loss, by $13,489,824 to $30,015,445 as at December 31, 2022, with an opening retained earnings impact at January 1, 2023 of $15,923,172.

On January 8, 2024, the Company announced that it has changed its auditor from Former Auditor to the Auditor effective December 20, 2023. On December 7, 2023, CPAB issued an enforcement report (the “Enforcement Report”) against the Former Auditor resulting from the CPAB Report with respect to the audit of the Company’s financial statements for the fiscal year ended December 31, 2022 (“2022 Statements”).

The Enforcement Report identified multiple significant inspection findings, each of which constitute a separate Violation Event (as defined in the Rules of CPAB) with respect to the Former Auditor. As a result of the CPAB Report, a remediation plan is required for the audit of the 2022 Statements. The Company has received information requests from the Former Auditor on its remediation plan, including third party confirmations from all of the Company’s digital asset custodians to confirm existence of the digital assets and fair market value, confirmations for all the private investments confirming the existence of the Company’s holdings and their latest financing details, management forecast files and schedules including all assumptions used in the goodwill impairment analysis, confirmation of exchange traded products, working papers on the calculation of staking and lending revenue, management fees and node revenue.

Director Appointments, NCIB, US Listing and Treasury Management

On October 29, 2024, the Company announced that Valour has successfully eliminated its outstanding debt following a final C$5.5 million (US$4 million) repayment completed on October 16, 2024.

On September 16, 2024, the Company announced that it filed a Form 40-F Registration Statement (“Form 40-F”) with the United States Securities and Exchange Commission (the “SEC”), in connection with its application to list the Common Shares on The Nasdaq Stock Market LLC (the “Nasdaq”). The listing of the Company’s common shares on the Nasdaq remains subject to the approval of the Nasdaq and the satisfaction of all applicable listing and regulatory requirements, including the Form 40-F being declared effective by the SEC.

On July 31, 2024, the Company announced the appointment of Andrew Forson to its board of directors. Andrew Forson is an experienced financial and risk engineer, software architect, and trust and estate practitioner. He serves as the Head of Ventures and Investments for the Hashgraph Group, the commercialization and enablement arm of Hedera, where he has been instrumental in driving strategic investments and fostering innovation in the digital asset sector.

On July 18, 2024, the Company announced that as part of its digital asset treasury strategy, it purchased an additional 94.34 BTC, bringing its total BTC holdings to 204.34 BTC. Additionally, the Company has acquired 12,775 SOL tokens and 1,484,148 CORE tokens, with plans to actively participate in CORE DAO’s staking facility.

On June 10, 2024, the Company announced that it has adopted Bitcoin as its primary treasury reserve asset and has purchased 110 Bitcoins to initiate this strategy.

8

On June 6, 2024, the Company announced a Normal Course Issuer Bid (“NCIB”) to buy back Common Shares through the facilities of Cboe Canada.

On May 7, 2024, the Company announced that it had fully repaid balances of US$6 million and US$13.5 million, which were secured by BTC and ETH collateral, respectively.

Fiscal 2023

Asset Management

On August 29, 2023, the Company announced that Valour launched three new products on the Nordic Growth Market Exchange (“NGM”). Valour Ethereum Zero EUR precisely tracks the price of ETH without charging management fees, making an investment in the world’s second largest digital asset easy, secure and cost-effective. Valour Solana EUR precisely tracks the price of SOL, the native cryptocurrency fuelling the Solana network. Marketed as one the fastest blockchains, Solana has more than 400 live projects spanning its DeFi, NFT, and Web3 ecosystem. Valour’s Solana ETP makes an investment in this leading decentralised platform cost-effective, simple and secure. Valour Digital Asset Basket 10 (VDAB10) tracks the performance of the top 10 largest digital assets based on market capitalisation with a maximum cap of 30% for any constituent. Valour’s VDAB10 ETP provides investors with a diversified and dynamic exposure to the ever-evolving crypto landscape in a trusted and secure manner.

On August 22, 2023, the Company announced that VDSL launched 1Valour Ethereum Physical Staking ETP. The 1Valour Ethereum Physical Staking ETP simplifies network participation for investors. With a fixed yield, undefined expiry and a 1.49% management fee, investors have the potential to earn passive returns, sidestepping the technical challenges involved with staking, and actively contributing towards the evolving decentralized finance landscape. Enhanced security measures including slashing insurance and full collateralization mean investors benefit from additional transparency and security measures.

On July 12, 2023, the Company announced that Valour launched its digital asset basket ETP - Valour Digital Asset Basket 10 (VDAB10) SEK. The Valour Digital Asset Basket 10 (VDAB10) ETP provides retail and institutional investors with trusted, secure, and diversified exposure to 10 of the largest cryptocurrencies by market capitalization. With a quarterly rebalancing, the multi-digital asset ETP enables investors to gain access to certain of the largest disruptive digital assets, offering an expanded entry into the rapidly developing digital asset ecosystem, without the need to set up a dedicated trading account.

On June 15, 2023, the Company announced that VDSL launched its first physically backed digital asset product, the 1Valour Bitcoin Physical Carbon Neutral ETP. The 1Valour Bitcoin Physical Carbon Neutral ETP provides investors with sustainable and climate-friendly exposure to Bitcoin with the low management fee of 1.49%. The ETP presents a trusted investment method that benefits the environment and aligns with environmental, social and governance (“ESG”) goals by funding certified carbon removal and offset initiatives in order to neutralise the associated Bitcoin carbon footprint.

On April 12, 2023, the Company announced the launch of VDSL, a Jersey-based securities issuer of ETPs for physically stored digital assets. VDSL obtained all regulatory approvals by the Swedish and Jersey regulators for an EU-wide offering to investors domiciled in Austria, Belgium, Croatia, Czech Republic, Denmark, Finland, France, Germany, Hungary, Ireland, Italy, Liechtenstein, Luxembourg, the Netherlands, Norway, Malta, Poland, Portugal, Romania, Slovakia and Spain, and its products will be listed on regulated stock exchanges such as Deutsche Börse/Xetra in Frankfurt, Euronext in Paris and Amsterdam and SIX Swiss Exchange in Switzerland.

9

On March 21, 2023, the Company announced the listing of certain ETPs on Euronext Paris, providing availability to French investors.

On January 23, 2023, the Company announced that on January 19, 2023, Genesis Global Capital LLC (“Genesis”) and its group companies filed for bankruptcy protection in the US and listed Valour as a creditor. Valour clarified that Valour Cayman, its wholly-owned subsidiary, is a borrower of funds under a master loan agreement with Genesis dated January 22, 2022. The loan amount borrowed by Valour Cayman under the loan agreement is US$6 million which is collateralised.

On January 10, 2023, the Company announced the approval of its renewed EU-base prospectus covering digital assets ETP-products by the Swedish Financial Supervisory Authority (“SFSA”).

Partnerships and Acquisitions

On December 18, 2023, the Company announced that it has entered into a definitive purchase agreement (the “Solana IP Agreement”) to acquire intellectual property (“Solana IP”) from prominent Solana developer Stefan Jørgensen (the “Solana IP Acquisition”). Pursuant to the Solana IP Agreement, the Company issued a total of 7,297,090 Common Shares at a deemed price of $0.55 per Common Share to Mr. Jørgensen in exchange for all of the Solana IP. The Payment Shares will be issued in five tranches over a period of two years, and be subject to the continued involvement of Mr. Jørgensen with the Company and its subsidiaries at the time of issuance. The Solana IP acquired by the Company encompasses a suite of sophisticated features including advanced liquidity provisioning, innovative trading strategies and technologies, along with the distribution, management, and analytics of decentralized financial data. These elements are tailored to support the Solana-focused trading desk operated by both the Company and Valour. The Solana IP Acquisition positions the Company to significantly elevate its capabilities, offering cutting-edge trading solutions and unique strategies specifically designed for Solana, a blockchain platform rapidly gaining recognition for its outstanding performance capabilities. The Solana IP Acquisition closed on February 9, 2024.

On October 24, 2023, the Company announced that it has entered into a joint venture agreement with Neuronomics AG (“Neuronomics”) to collaborate on the development of AI based exchange traded products, actively managed certificates, and asset backed tokens for global distribution. To further align the interests of the Company and Neuronomics, the Company entered into share exchange agreements with Olivier Roussy Newton, Chief Executive Officer of the Company and Johan Wattenstrom, Director of Valour, pursuant to which DeFi acquired from each of Mr. Newton and Mr. Wattenstrom 362 shares of Neuronomics with nominal value of CHF 1.- for a total of 724 shares of Neuronomics.

Management, Board, Auditor Changes and Name Change

On January 8, 2024, the Company announced the change of its auditors from BF Borgers CPA PC to HDCPA Professional Corporation effective December 20, 2023.

On July 7, 2023, the Company announced that it had changed its name from “Valour Inc.” to “DeFi Technologies Inc.”

On February 13, 2023, the Company announced that Russell Starr has elected to step down from his role as Executive Chairman but will remain as Head of Capital Markets. Olivier Francois Roussy Newton, CEO of Valour, assumed the role of Executive Chairman replacing Russell Starr.

On February 3, 2023, the Company announced the change of its auditors from RSM Canada LLP to BF Borgers CPA PC.

10

Financings

On November 13, 2023, the Company announced a non-brokered private placement financing of up to 6,250,000 units (a “Unit”) at a price of $0.16 per Unit (the “Unit Price”) for gross proceeds of up to $1,000,000 (the “Nov 2023 Offering”). Each Unit consisted of one common share of the Company (a “Unit Share”) and one common share purchase warrant (a “Warrant”), entitling the holder to acquire one additional common share of the Company (a “Warrant Share”) at an exercise price of $0.23 for a period of 24 months from issuance. The Nov 2023 Offering closed on an oversubscribed basis for 11,812,500 Units, representing aggregate gross proceeds of $1,890,000.

On November 1, 2023, the Company announced that Valour completed a non-brokered private placement financing of unsecured convertible notes (the “Notes”) for gross proceeds of C$3,000,000 (the “Convertible Offering”). The Notes issued in connection with the Convertible Offering accrue interest at a rate of 8% per annum and will mature on October 31, 2025 (“Maturity Date”). Upon the occurrence of certain trigger events, the principal amount of Notes and all accrued interest may be convertible (a “Conversion”), at the option of the holder, into (a) Common Shares (“Conversion Shares”) at a price of C$0.10 (“Conversion Price”) per Conversion Share and (b) an equal number of common share purchase warrants of the Company (“Conversion Warrants”) entitling the holder to acquire Common Shares at a price of C$0.20 for a period of five years from the date of issuance. Upon the Conversion, the Company will subscribe for such additional equity of Valour equal to the principal amount of Notes and accrued interest converted pursuant to the Conversion. As of the date hereof, all of the Notes were converted into Conversion Shares and Conversion Warrants.

On August 23, 2023, the Company announced that it has entered into shares for debt settlement agreements with a lender, an officer and consultants of the Company to settle an aggregate amount of approximately C$604,543.34 of accrued debt obligations and accrued fees owing to such lender, officer and consultants of the Company by issuing Common Shares at a price of C$0.105 per Common Share for a total of 5,757,827 Common Shares.

On June 30, 2023, the Company announced that it filed a preliminary short form base shelf prospectus (the “Preliminary Base Shelf Prospectus”) with the securities regulators in each province and territory of Canada. The filing of the Preliminary Base Shelf Prospectus was subsequently withdrawn.

On June 12, 2023, the Company announced that it entered into shares for debt settlement agreements with various officers and consultants of the Company to settle an aggregate amount of approximately C$674,837.78 of accrued fees owing to such officers and consultants of the Company by issuing Common Shares at a price of C$0.085 per Common Share for a total of 7,939,268 Common Shares.

Fiscal 2022

Management, Board and Advisory Board Changes

On November 14, 2022, the Company announced the resignation of Bernard Wilson as director of the Company.

On October 6, 2022, the Company announced the appointment of Olivier Roussy Newton as Chief Executive Officer of the Company following the resignation of Russell Starr. In addition, the Company announced Russell Starr will re-assume the role of Head of Capital Markets and maintain his role as Executive Chairman of the Company.

On July 5, 2022, the Company announced Diana Biggs stepped down from her role as Chief Strategy Officer of the Company.

Financings

On November 29, 2022, the Company announced the closing of the second tranche of the October 2022 Unit (as defined below) offering for gross proceeds of $132,400 through the sale of 662,000 October 2022 Units. No finders fees were paid in connection with the closing of the second tranche. The securities underlying the second tranche closing were subject to a statutory hold period of four months and one day following the closing date, which expired on March 30, 2023.

11

On November 14, 2022, the Company announced the closing of the first tranche of the October 2022 Unit offering, for gross proceeds of $1,414,973 through the sale of 7,074,865 October 2022 Units. A director of the Company purchased 2,500,000 October 2022 Units under the first tranche closing. In connection with the November 14, 2022 first tranche closing of the October 2022 Unit offering, the Company paid aggregate finder’s fees of C$ 7,499.73 in cash to certain finders and 187,493 broker warrants, each broker warrant entitling the holder to acquire one Share at a price of $0.30 for a period of two years from issuance. The securities underlying the first tranche closing were subject to a statutory hold period of four months and one day following the closing date, which expired on March 15, 2023.

On October 11, 2022, the Company announced its non-brokered private placement financing of 25,000,000 units (the “October 2022 Units”), at an offering price of $0.20 per October 2022 Unit, for aggregate gross proceeds of $5,000,000. Each October 2022 Unit was comprised of one Common Share and one-half Common Share purchase warrant, entitling the holder of a whole warrant to acquire one Common Share, at an exercise price of $0.30, for a period of 24 months from issuance.

SEBA Bank Partnership and Investment

On January 25, 2022, the Company announced that it closed its investment of CHF 25 million in SEBA, acting as the co-lead in the oversubscribed CHF 110 million Series C funding round of SEBA. SEBA is a fully integrated, Swiss Financial Market Supervisory Authority (“FINMA”) licensed, digital assets banking platform providing a seamless, secure, and easy-to-use bridge between digital and traditional assets.

On January 5, 2022, the Company announced that it has entered into a commercial agreement (the “Preferred Partnership Agreement”) to establish a preferred partnership relationship with SEBA. The Preferred Partnership Agreement outlines a framework for the Company to become a preferred provider of staking services, client referrals, market making and liquidity to SEBA, and SEBA to become a preferred provider of custody services to the Company. The Preferred Partnership Agreement also outlines further cooperation between SEBA and the Company with respect to asset and investment management, mining services, tokenization, digital capital markets and institutional research.

Additions to Indices

On January 26, 2022, the Company announced that it will be added to the CoinShares Blockchain Global Equity Index, administered by Solactive AG, on February 8, 2022. The index aims to offer exposure to listed companies that participate or have the potential to participate in the blockchain or cryptocurrency ecosystem. It also aims to capture the potential investment upside generated by earnings related to the adoption of blockchain technologies or cryptocurrencies.

On January 24, 2022, the Company announced that it has been added to the Melanion Bitcoin Exposure Index. This unique index, sponsored by Melanion Capital and administered by Bita GmbH, marks the first milestone in the development of an innovative Digital Asset business for Melanion Capital.

ESG Initiatives

On January 18, 2022, the Company announced that it joined the Crypto Climate Accord, an industry initiative whose objective is to decarbonise the global crypto industry by prioritizing climate stewardship and supporting the entire crypto industry’s transition to net zero greenhouse gas emissions by 2040, as a supporter.

12

Asset Management

On December 23, 2022, the Company announced its products were listed on the independent comparison platform MoneyMoon, a major European ETP comparison platform.

On December 1, 2022, the Company announced its partnership with Autostock, a Swedish trading platform, to launch an automated trading strategy designed to capture weekly effects of Bitcoin.

On October 28, 2022, the Company announced it had filed a new EU-base prospectus covering digital assets ETP-products with the SFSA.

On October 18, 2022, the Company announced the consolidation of its full pro-rated ETHW allocation received as a result of the Ethereum proof-of-work to proof-of-stake forking event. Net proceeds from the consolidation were reinvested into the underlying asset of the Company’s Ethereum Zero certificate products. The change was reflected through an adjustment to the net asset value of both Valour Cayman Ethereum Zero certificates (SEK and EUR denominated).

On October 12, 2022, the Company announced its partnership with Swedish index provider Vinter to launch the Company’s first multi-asset crypto ETP, the Valour Digital Asset Basket 10 ETP (VDAB10). The Valour Digital Asset Basket 10 ETP tracks the 10 largest digital assets weighted by their market capitalisation, with a maximum portfolio allocation of 30% per asset.

On September 23, 2022, the Company announced the debut and trading of its Carbon Neutral Bitcoin ETP on the Boerse Frankfurt Zertifikate AG (the “Frankfurt Exchange”).

On August 24, 2022, the Company announced the debut and trading of its new Binance Coin Exchange traded product, Valour (BNB) EUR ETP, on the Frankfurt Exchange. The Valour (BNB) EUR ETP tracks the price of BNB, the native token behind the BNB Chain, a decentralized open-source, multi-chain platform being used to build parallel virtual ecosystem infrastructure.

On August 18, 2022, the Company announced an agreement with German banks, Comdirect and Onvista, that will enable banking clients to integrate Valour Cayman ETPs into their investment portfolios.

On August 16, 2022, the Company announced its partnership with German online brokerage firm justTrade, whereby the Company was retained to provide physically-backed crypto ETPs to justTrade’s savings plan program (Sparplan) by the end of the year.

On July 26, 2022, the Company announced trading of its ETP products on the Lang and Schwarz Exchange, based in Germany. Trading of Bitcoin Zero, Etherium Zero, Valour Uniswap ETP, Valour Polkadot ETP, Valour Cardano ETP, Valour Solana ETP, Valour Avalanche ETP, and Valour Cosmos ETP began July 25, 2022.

On May 26, 2022, the Company announced Valour Cayman received approval to begin trading of the Valour Enjin (ENJ) EUR ETP and Valour Cosmos (ATOM) EUR ETP on the Frankfurt Exchange. Trading began on May 26, 2022.

On May 2, 2022, the Company announced that Valour Cayman received approval from the SFSA to extend its distribution from the Top 75 single digital assets by market capitalization to the Top 125.

On April 6, 2022, the Company announced that Valour Cayman began trading of its Polkadot (DOT) EUR ETP, Cardano (ADA) EUR ETP, and Solana (SOL) EUR ETP on the Euronet Exchange in Paris and Amsterdam. Trading began on April 6, 2022.

On February 17, 2022, the Company announced a strategic partnership with RockX, a Singapore-based institutional gateway to crypto finance and blockchains, to enhance the staking components of the Company’s current respective ETP infrastructures, co-develop ETP products, provide institutional staking services, custodian services and real time data yield oracle.

13

On February 16, 2022, the Company announced that Valour Cayman received approval to begin trading of its Terra (LUNA) SEK ETP and Avalanche (AVAX) SEK ETP on the Nordic Growth Market Exchange (“NGM”). Trading on the NGM began on February 28, 2022 and trading on the Frankfurt Exchange began on March 25, 2022.

On February 14, 2022, the Company announced that Valour Cayman received approval to begin trading of the Polkadot (DOT) EUR ETP and Cardano (ADA) EUR ETP on Frankfurt Stock Exchange. Trading began on February 21, 2022.

On February 2, 2022, the Company announced that Valour Cayman applied for a Swiss Verein zur Qualitätssicherung von Finanzdienstleistungen (“VQF”) membership through its Swiss subsidiary Valour Europe AG (formerly known as DeFI Europe AG). The VQF membership is awarded by the Verein zur Qualitätssicherung von Finanzdienstleistungen (Financial Services Standards Association), a self-regulatory association for the financial industry in Switzerland. Approval for the VQF membership was granted on April 11, 2022.

On February 1, 2022, the Company announced that Valour Cayman received approval to begin trading its Solana ETP on the Frankfurt Exchange, with trading to begin February 2, 2022.

Ventures

On April 5, 2022, the Company announced it had participated in the $45 million Series A raise for Boba Network, a blockchain Layer-2 scaling solution and Hybrid Compute platform that integrates smart contracts with Web2 API.

On January 19, 2022, the Company announced that it has made a block purchase of $WILD tokens, the native token of Wilder World, an immersive 5D Metaverse built on Ethereum, Unreal Engine 5 and open protocol ZERO.

Normal Course Issuer Bid

On April 8, 2022, the Company announced the extension of its Normal Course Issuer Bid (“NCIB”), previously launched on April 13, 2021, to buy back Common Shares through the facilities NEO Exchange and/or other Canadian alternative trading platforms. The actual number of Common Shares that may be purchased under the NCIB and the exact timing of such purchases will be determined by the Company. Under the terms of the NCIB, the Company may, if considered advisable, purchase its Common Shares in open market transactions through the facilities of the NEO Exchange and/or other Canadian alternative trading platforms not to exceed up to 10% of the public float for the Common Shares as of April 8, 2022, or 20,359,513 Common Shares, purchased in aggregate. The price that the Company will pay for the Common Shares shall be the prevailing market price at the time of purchase and all purchased Common Shares will be cancelled by the Company. In accordance with NEO Exchange rules, daily purchases (other than pursuant to a block purchase exception) on the NEO Exchange under the NCIB cannot exceed 25% of the average daily trading volume on the NEO Exchange as measured from November 8, 2021 to April 8, 2022.

14

DESCRIPTION OF THE BUSINESS

General

The Company is a publicly listed issuer on Cboe Canada trading under the symbol “DEFI”. The Company is a technology company bridging the gap between traditional capital markets and decentralized finance through five primary business lines:

| ● | Asset Management – Valour develops and lists ETPs traditional exchanges in Europe that provide indirect exposure to underlying digital assets, digital asset indexes, or other decentralized finance instruments; |

| ● | Ventures – The Company make early-stage investments in companies, banks and foundations in the digital asset space; |

| ● | DeFi Alpha – The Company operates a specialized arbitrage trading desk based in Switzerland that focuses on identifying and capitalizing on low-risk arbitrage opportunities within the digital asset market; |

| ● | Reflexivity Research – Reflexivity is a private research firm that specializes in producing research reports on digital assets. |

| ● | Stillman Digital – Sillman is an OTC desk and digital asset liquidity provider, in October 2024. |

“Decentralized finance” or “DeFi” refers to a financial system that seeks to operate as an alternative to the traditional financial system. DeFi seeks to allow people and companies to effect transactions on a “peer to peer” basis, typically employing blockchain or other distributed ledger technology to allow participants to interact with one another directly between each other. Because transactions are effected peer to peer, DeFi does not rely on traditional intermediaries such as banks, brokerages, and stock exchange, so transactions can be completed on a more timely basis and without the fees typically charged by intermediaries.

Asset Management

Valour ETPs

The Company’s wholly owned subsidiary Valour Cayman develops and lists ETPs on regulated stock exchanges and multilateral trading facilities in Europe that synthetically track the value of digital assets, or an index or basket thereof. ETPs simplify the ability for retail and institutional investors to gain exposure to cryptocurrencies and decentralized finance as they remove the need to manage wallets, various logins, custody and other intricacies that are linked to managing a digital asset portfolio. Rather, retail and institutional investors can simply purchase the associated ETP with the digital asset they wish to gain exposure to through a bank or brokerage account with access to the relevant stock exchanges and multilateral trading facilities.

As of the date hereof, Valour Cayman has listed 55 ETPs. Valour Cayman currently lists its ETPs, on the following European stock exchanges: Spotlight Exchange, Deutsche Börse Xetra, Gettex, Frankfurt Exchange, Euronext Amsterdam, Euronext Paris and Lang and Schwarz Exchange. The listing of ETPs are subject to exchange approval by the relevant exchange. A full list of ETPs listed by Valour Cayman can be found here: https://valour.com/en/products.

Products and Services

Valour Cayman ETPs are issued under a base prospectus dated March 16, 2021 (as amended and updated to the date hereof, the “Base Prospectus”), as supplemented by supplements or final terms from time to time (“Final Terms”), which together govern the ETP program (the “Program”). The Base Prospectus has been approved by the SFSA, the Swedish financial authority, and is passport eligible in Austria, Belgium, Denmark, Finland, France, Germany, Italy, Luxembourg, the Netherlands, Norway and Spain and/or, subject to completion of relevant notification measures, any other member state within the European Economic Area (“EEA”). For further details on the terms and conditions of the ETPs, a copy of the Base Prospectus may be obtained at https://www.fi.se/en/our-registers/prospektregistret/details/?id=24-34625.

15

Valour Cayman’s current ETP range are all open-ended certificates that provide exposure to a single digital asset, or an index or a basket thereof, as specified in the relevant Final Terms. The Final Terms and for each of Valour Cayman’s ETPs are available on the company website on the respective ETP pages: https://valour.com/products. Valour Cayman is the issuer of the ETPs offered under the Program and also acts as calculation agent.

Valour Cayman’s policy is always to hedge substantially 100% of the market risk in the underlying asset. Hedging is primarily done continuously through an in-housed developed auto-hedger and in direct correspondence to the issuance of ETPs to investors, but Valour Cayman may elect to utilize other hedging methods it deems appropriate. In order to hedge its exposure to each digital asset, Valour Cayman relies on cryptocurrency exchanges and counterparties to be able to buy and sell the digital assets, or interests in funds that hold digital assets, which the ETPs track.

For its Bitcoin Zero and Ethereum Zero products, Valour Cayman charges zero management fees and for all other products, a management fee of 1.9% to 2.5% applies.

Valour Digital Securities Limited ETPs

VDSL is a special purpose vehicle incorporated as a public limited liability company under the laws of Jersey. VDSL is owned by the charitable trust VLR Charitable Trust in Jersey. In April 2023, VDSL obtained all regulatory approvals by the Swedish and Jersey regulators for an EU-wide offering of physically backed ETPs to investors domiciled in Austria, Belgium, Croatia, Czech Republic, Denmark, Finland, France, Germany, Hungary, Ireland, Italy, Liechtenstein, Luxembourg, the Netherlands, Norway, Malta, Poland, Portugal, Romania, Slovakia and Spain. Valour Cayman acts as arranger for all ETPs issued by VDSL.

As of the date hereof, Valour Cayman has listed 6 ETPs. VDSL ETPs are currently listed on the Deutsche Börse Xetra and Euronext Amsterdam. The listing of ETPs are subject to exchange approval by the relevant exchange.

Products and Services

VDSL ETPs are issued under a base prospectus dated April 24, 2024 (the “VDSL Base Prospectus”), as supplemented by supplements or final terms from time to time (“VDSL Final Terms”), which together govern the VDSL ETP program (the “VDSL Program”). The VDSL Base Prospectus has been approved by the SFSA, the Swedish financial authority, and is passport eligible in Austria, Belgium, Croatia, Czech Republic, Denmark, Finland, France, Germany, Hungary, Ireland, Italy, Liechtenstein, Luxembourg, the Netherlands, Norway, Malta, Poland, Portugal, Romania, Slovakia and Spain. VDSL may also request the SFSA to publicize the approval of the VDSL Base Prospectus to other EEA states in accordance with Regulation (EU) 2017/1129. In addition, VDSL may decide to register this VDSL Base Prospectus in Switzerland with the reviewing body SIX Exchange Regulation AG or another FINMA approved reviewing body, as a foreign prospectus that is also deemed to be approved in Switzerland pursuant to Article 54 paragraph 2 FinSA, for the purposes of making a public offer of VDSL ETPs in Switzerland or admission to trading of all or a series of VDSL ETPs on a regulated stock exchange in Switzerland. For further details on the terms and conditions of the ETPs, a copy of the VDSL Base Prospectus may be obtained at https://www.fi.se/en/our-registers/prospektregistret/details/?id=24-5713.

The VDSL Program permits VDSL to issue VDSL ETPs related to any one of 124 underlying digital currencies (“Digital Currencies”) (or more subject to supplements to the VDSL Base Prospectus), to a “basket” comprising two or more of such Digital Currencies or to an index linked to Digital Currencies, as specified in the relevant VDSL Final Terms. The VDSL Final Terms and for each of VDSL’s ETPs are available on the company website on the respective ETP pages: https://valour.com/products. The VDSL ETPs are designed to offer investors a means of investing in Digital Currencies without having to acquire digital assets themselves and to enable investors to buy and sell that interest through the trading of a security on a stock exchange.

Each VDSL ETP is an undated secured limited recourse debt obligation of VDSL, which ranks equally with all other VDSL ETPs of the same class. VDSL ETP holders only have recourse to the assets of the class of VDSL ETP of which they are a holder. If the net proceeds are insufficient for VDSL to make all payments due, neither the trustee nor any person acting on behalf of the trustee will be entitled to take any further steps against the VDSL, and no debt shall be owed by the VDSL in respect of such further sum.

16

The underlying assets for the VDSL ETP of each class, by which they are backed and on which they are secured, comprise private keys evidencing ownership of Digital Currencies. These private keys are held in the name of VDSL in secure vaults at the premises of the relevant custodian of VDSL (“VDSL Custodian”) and are not fungible with other digital assets held by the relevant VDSL Custodian.

The VDSL ETPs are constituted under the trust instrument dated April 5, 2023 between VDSL and The Law Debenture Trust Corporation p.l.c. as trustee (the “Trustee”) for the holders of VDSL ETPs (“VDSL ETP Holders”) (the “Trust Instrument”). The Trustee holds all rights and entitlements under the Trust Instrument on trust for VDSL ETP Holders. In addition, VDSL and the Trustee have entered into a single security deed (the “Security Deed”) in respect of all pools of VDSP ETPs (“Pools”). The rights and entitlements held by the Trustee under the Security Deed, to the extent attributable to a Pool, are held by the Trustee on trust for the VDSL ETP Holders of that particular class of VDSL ETP. Under the terms of the Security Deed, VDSL has charged to the Trustee for the benefit of the Trustee and the relevant VDSL ETP Holders by way of first fixed charge the Digital Currencies held in custody attributable to the relevant class of VDSL ETP and all rights of VDSP in respect of the respective custody accounts to the extent attributable to the relevant Pool. VDSL has also, under the terms of the Security Deed, assigned to the Trustee by way of security the contractual rights of the issuer relating to such class under the custody agreements entered into by VDSL and has granted a first-ranking floating charge in favour of the Trustee over all of VDSL’s rights in relation to the secured property attributable to the applicable Pool, including but not limited to its rights under the custody agreements and the custody accounts attributable to that Pool.

VDSL charges management fees ranging from 1.9% to 2.5% on the VDSL ETPs.

Staking of Cryptocurrency and Defi Protocol Tokens

As part of Valour’s policy to hedge substantially 100% of the market risk, Valour purchases and sells the digital assets, and investments exposed to digital assets, which its ETPs track. Valour may trade, lend or stake such digital assets on its balance sheet to generate revenue in accordance with the policies in the Base Prospectus of Valour Cayman and as Staking Agent for VDSL in accordance to VDSL’s base prospectus. Lending or staking transactions are only conducted with institutional-grade counterparties and only up to a certain percentage for risk management purposes in accordance with Valour’s Lending and Staking Policy.

Pursuant to the Lending and Staking Policy, lending and staking activities are overseen by the Head of Asset Management and Trading (“CIO”), Head of Finance (“CFO”) and the director of Valour. Prior to entering into any lending or staking transaction, due diligence will be conducted on all potential counterparties, and in particular counterparties in the following situations:

| ● | Custody of assets of Valour by third parties, without legal separation from assets of such third party |

| ● | Deposits of cash with banks and investment firms |

| ● | Bilateral FX transactions (settlement risk) |

| ● | Bilateral transactions in digital assets (settlement risk) |

| ● | Lending and borrowing transactions relating to digital assets (settlement risk) |

17

In order to evaluate a counterparty the following information is collected and documented in the counterparty scorecard:

Contact information

The name, the website and contact person at the exchange/counterparty, as well as the responsible onboarding owner on Valour side.

Current status

The current status of the relationship, the connection type, as well as the services, products and currency pairs used on the respective exchange/counterparty have to be documented and kept up to date.

Country of registration and regulation

The country in which the exchange/counterparty is registered must be documented. In addition all countries in which the exchange/counterparty holds a regulatory licence have to be assessed and documented by stating the licence number (if applicable).

Country risk

The country of registration as well as the country/-ies of regulation are evaluated by using the country risk matrix. The country risk matrix considers the FATF (and equivalent) country evaluation, the Transparency.org Corruption Perception Index (CPI) as well as the VQF SRO country risk recommendations.

Adverse media search

An adverse media search is being conducted. For example, information about an exchange having been hacked in the past or any news about a negative reputation, regulatory breaches etc are documented.

Public exchange scores

Publicly available information and risk scores from data sources such as Coinmarketcap and Coingecko are being collected and documented.

Information security certification

The exchange/counterparty information security certification status is assessed. Information about the possession of certifications such as AICPA SOC 1, SOC 2 Type I and SOC 2 Type II as well as ISO 27001 are documented.

Insurance coverage

Information about insurance protection and regulatory status in terms of investor protection are assessed and documented.

Proof of reserves

It is being checked if the exchange/counterparty has made the public wallet addresses of its cold and hot storage publicly available or if any other cryptographic means of verification of the reserves held in custody are either publicly available or have been audited.

Risk evaluation

The risk score is evaluated on a scale of 1 to 5, with 1 being the lowest risk and 5 being the highest risk. Based on the information collected in the scorecard, with a focus on regulatory licences, a risk score is calculated and documented for each exchange or counterparty.

18

Business justification and restrictions

In cases where an exchange or counterparty presents increased risks, a business justification must be provided. Any decision to establish a business relationship with an exchange or counterparty with increased risks must be approved by the board.

Recurring review schedule

The review date and review frequency of all exchanges/counterparties are documented and tracked in the scorecard. A review once a year is set as the default standard, however, an ad-hoc review has to be considered in case of any event that may result in any of the assessment criteria being changed.

Account closure

If the exchange or counterparty has been identified with an increased risk, such as a risk score of 4 or 5, Valour will determine if it is necessary to close the business relationship. This decision is based on the potential exposure and the potential impact on the business and stakeholders. If it is determined that the business relationship should be terminated, a plan for closing the relationship is developed in a controlled and orderly manner. This may include transferring outstanding transactions, closing accounts, and ensuring that all necessary documents and records are properly transferred or retained. The decision to close the business relationship is communicated to the exchange or counterparty and a timeline for the closure is provided. Once the business relationship has been successfully terminated, the counterparty scorecard is updated in order to reflect the closure.

When deciding whether to lend or stake a particular asset, the Lending and Staking Policy provides that the decision will initially be made based on the risk profile of the potential counterparties, then the highest yield available, then prioritizing staking over lending.

The Lending and Staking Policy also sets limits on how much of a particular digital asset can be lent or staked of 55% in the case of assets under management of less than US$10 million, and 80% for over US$10 million. Allocations by counterparty will be limited to 33% of Valour Cayman’s aggregate assets. Exceptions to these rules can be made with Valour Board approval.

“Staking” refers to the process of dedicating digital assets to a particular blockchain for a set period of time so as to verify transactions on that blockchain. The act of staking typically results in the staking person or company receiving newly-created digital assets of the same type as a reward verifying the transactions. In addition, having digital assets staked improves the integrity and security of the applicable blockchain ledger.

Custody of Digital Assets

The policies of Valour require the application of internal multi-signature cold-storage and external custody. External custody solutions include specialized third-party custody providers within the United States and Europe. Valour currently utilizes the following third-party custody providers to hold and safeguard Valour’s digital assets:

| Custodian | Location | % of digital assets custodied by market value(1) | Regulatory Body | |||

| Binance | Cayman Islands | 15.3% | Cayman Islands Monetary Authority (CIMA) | |||

| B2C2 Overseas LTD | Cayman Islands | 0.8% | Cayman Islands Monetary Authority (CIMA) | |||

| Bitcoin Suisse AG | Switzerland | 0.0% | Financial Services Standards Association (VQF). Zug. Switzerland | |||

| Kraken | United States | 0.1% | Office of Comptroller of Currency | |||

| Anchorage Digital | United States | 0.0% | Office of Comptroller of Currency | |||

| Laser Digital | Switzerland | 0.8% | Financial Services Standards Association (VQF). Zug. Switzerland |

19

| Copper | Switzerland | 7.1% | Financial Services Standards Association (VQF). Zug. Switzerland | |||

| Fund A(2) | United States | 20.4% | Office of Comptroller of Currency | |||

| Fund B(2) | United States | 11.1% | Office of Comptroller of Currency | |||

| Wintermute | United Kingdom | 0.0% | Financial Conduct Authority (FCA) | |||

| Bitgo Trust | United States | 0.5% | South Dakota Division of Banking and Money Services Business (MSB) with Financial Crimes Enforcement Network (FinCEN) |

Note 1: As at December 31, 2024; Residual digital assets served as collateral for loans with Genesis Global Capital LLC (0.04%; subject to bankruptcy proceeding/filing as of January 19, 2023).

Note 2: The Company’s hold interest in funds that acquired Solana and Avalanche tokens from a bankrupt company. The Company has included these positions in this chart to illustrate the underlying Solana and Avalanche tokens held in such funds.

VDSL

| Custodian | Location | % of digital assets custodied by market value(1) | Regulatory Body | |||

| Copper Markets (Switzerland) AG | Switzerland | 100% | Financial Services Standards Association (VQF), Zug, Switzerland | |||

| Komainu (Jersey) Limited | Jersey | 0% | Jersey Financial Services Commission |

Note 1: As at December 31, 2024;

Prior to engaging any prospective third-party to perform custody services, Valour conducts diligence and counterparty risk analysis of such third-party. Such measures include:

| ● | verifying contact information of the third-party and the responsible onboarding owner on the Valour Cayman side. |

| ● | reviewing current status of the relationship with the third-party, the connection type, as well as the services, products and currency pairs used by the third-party. |

| ● | documenting the prospective third-party’s regulatory regime and licenses. |

| ● | assessing the third-party’s jurisdiction of incorporation and regulatory regime for compliance to international anti-terrorism and money laundering guidelines such as the Financial Action Task Force country evaluation, Transparency.org Corruption Perception Index as well as the VQF SRO country risk recommendations. |

| ● | collecting and documenting public exchange scores, such as Coinmarketcap and Coingecko, of the third-party |

| ● | assessment of the third-party’s information security certification, such as AICPA SOC 1, SOC 2 Type I and SOC 2 Type II as well as ISO 27001. |

| ● | assessment and documentation of the third-party’s insurance coverage with respect to investor protection. |

| ● | verifying if the third-party has made the public wallet addresses of its cold and hot storage publicly available or if any other cryptographic means of verification of the reserves held in custody are either publicly available or have been audited. |

| ● | searching for any adverse public media results regarding the third-party |

| ● | analyzing risk exposure and business restrictions through engaging the third-party. |

| ● | recurring review of third-party custody providers. |

20

Valour’s current third-party custody providers do not engage sub-custodians to provide custody services. None of Valour ’s current third-party custody providers are Canadian financial institutions or related parties of the Company. Each of Valour’s third-party custody providers maintain general commercial insurance on its own behalf and would be subject to their respective jurisdiction’s bankruptcy laws in the event of such an event. The Company and Valour are not aware of any aspect of the above custody providers that would adversely affect the Company from obtaining an unqualified audit opinion on its audited financial statements. The Company and Valour are not aware of any security breaches or similar incidents with respect to its third-party custody providers.

In addition, Valour utilizes custody solutions offered by institutional quality exchanges. The exchanges typically store between 95% and 100% of the assets in multi-signature cold storage. Different exchanges store different proportions of their assets in online wallets, and the proportion of assets in cold storage is one of the factors determining their risk weight in our model for capital adequacy. Cold storage means storage facilities where the private keys of a wallet are held off-line protected physically as well as by the multi-signature features of the wallet. By comparison, hot storage means storage facilities or platforms that are connected to the internet, which provide greater accessibility to digital assets for users, but are subject to greater cybersecurity risks.

The Company does self custody some of the Company’s portfolio using meta mask and other hot wallets. The total value of the Company’s digital assets under self custody was approximately $488.4 M on December 31, 2024 (December 31, 2023 – approximately $4.5M). Some digital assets related to the Valour Cayman ETPs are self-custodied.